Why Roth IRA for Your Kid Is a Good Investment?

I know for a kid retirement may be a strange concept; however, investing your kids “earned income” using an Individual Retirement Account (IRA) is the best financial decision. For instance, if you kid made money by doing office work, modeling, data entry, any other part-time work and earned income, the kid is qualified to contribute to an IRA. In particular, Roth IRA is the best for a kid because of tax-free growth.

Who is eligible?

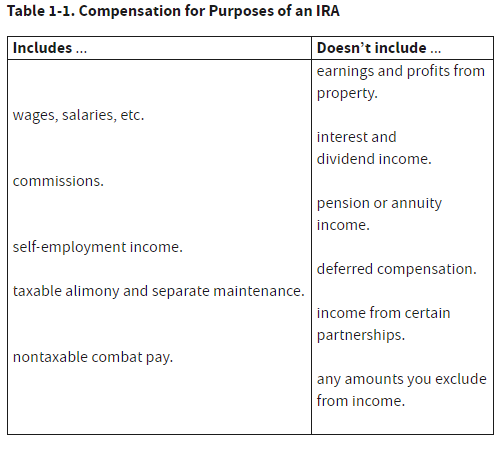

Although, there is no minimum age limit to contribute to Roth IRA for a kid; he or she must have earned income. For instance, your toddler modelling for your own business to your teen teaching (tution), working in a restaurant or a grocery store, or babysitting qualify as long as he or she has “employment compensation”. Below is the compensation table from IRS publication 590-A.

So as long as your kid earns income from a job (wages, salaries) or has self-employment income, he or she is qualified to contribute to Roth IRA.

Contribution Limit

The maximum contribution limit to Roth IRA is $6,000 in 2021 ($7,000 if you are 50 or above). Your kid can either contribute up to the maximum amount or up to his or her earned income of the year whichever is less.

Although there is no age limit, there is an income limit. For instance, you can contribute to a Roth IRA only if your Adjusted Gross Income (AGI) is less than $140,000 for a single filer in 2021. In most cases, your kid would meet the income criteria to contribute to Roth IRA. If not, it is a good problem, right! You will need a whole new strategy!

Benefits of Roth IRA

Tax-Free Growth

One of the benefits of Roth IRA is “tax-free” growth. Remember, you fund Roth IRA with your after-tax money, meaning you already paid tax on money contributed to Roth IRA. Now your contribution and earnings grow tax free. After age 59 ½, all the money in a Roth IRA is yours, tax-free! Moreover, there is no mandatory distribution such as Required Minimum Distribution (RMD). So your investment continues to grow tax-free until you decide to take money out of your Roth IRA account!

Penalty-Free Withdrawal

Yet another benefit of Roth IRA is that you can withdraw your contributions any time without any tax consequences or penalty. There is no restriction on the use of money either. Your kid can buy a video game or a car or pay for college expenses.

Not counted as asset on FAFSA

The value of your kid’s Roth IRA will not affect their financial aid eligibility. In fact, retirement account balances in your name or your kid’s name are not reported as assets on Free Application for Federal Student Aid (FAFSA).

Time is on your side

Two of the most important variables in investment are time horizon and risk. For a younger individual, both are in his or her favor. Instead of a typical 30 to 40 years time horizon for an adult, your kid may have a much longer investment time horizon. The longer time horizon would allow you to take more risk and your investment will have more time to compound.

If you really want to sell this to your kid, show him or her the following picture:

Annual Contribution:$3,000 from age 14 to 18

Total Contribution: $12,000

Annual compounding at 10%*

*The historical rate of return for S&P 500 from 1970 to 2020 with dividend reinvested is 10.67%.

After 50 years, the value of the account is $1,227,973 (not adjusted for inflation), out of which $1,215,973 is due to compounding!!!

Assuming 3% average inflation over 50 years, the inflation adjusted amount is $280,109, still a significant amount compared to the total of $12,000 contribution.

The beauty of it all is that your kid may not have to pay any taxes at all during his or her lifetime for qualified withdrawal..

I am sure this will get your kid interested!

Education at young age

We know that investment in the equity market is not without risk. Your kid’s Roth IRA if invested in equity may lose money (on paper); however, the history indicates that it is unlikely over a long investment time horizon. Although past performance is not a guarantee of future results, the historical data from 1970 to 2020 shows that, with all of the booms and busts of the equity market, the annualized real return (adjusted for inflation) of S&P 500 (including dividend reinvestment) is 7.56% (well above average inflation rate of 2% to 3%).

This will be a great lesson for your kid as he or she will learn the concept of long-term investing, compounding growth, inflation risk, and staying the course.

Investment for Roth IRA

Most large brokerage firms such as Vanguard, Fidelity, Schwab offer Roth IRA for minors. You will have to serve as custodian of the account until your minor reaches the required age of majority which is typically 18 years in most states. At that time, your child will be in control of his or her Roth IRA. He or she can take all money out or stay invested, you have no control over his or her Roth IRA.

Since your minor will have decades of investment time horizon, consider a 100% equity portfolio. For example, 100% of money can be invested in Vanguard Total Stock Market Index Fund (VTSAX) or Vanguard Small-Cap Index Fund (VSMAX) or combination of the two. You can further diversify with adding Vanguard Total International Stock Index (VTIAX). I would generally stick with broadly diversified index funds.

Summary

If your child has earned income, consider opening a Roth IRA for your kid. Besides tax advantages such as tax-free growth and not subject to RMD, it will be a great educational experience for your kid.

Get out next article in your inbox.