Backdoor Roth IRA: Step-By-Step Guide

Who does not like tax-free growth, not pay any taxes on withdrawals including contributions and earnings ever, and not forced to take money out of the retirement account ever? The Roth IRA gives you such benefits. However, there is an income limit. For instance, you can contribute to a Roth IRA only if your Adjusted Gross Income (AGI) is less than $140,000 for a single filer and $208,000 for married couples in 2021. Well, this is a good problem to have!

The good news is, there is no income limit for converting traditional IRA to a Roth IRA due to a rule change in 2010. The process is called backdoor Roth IRA. In nutshell, you contribute $6,000 to a traditional IRA first and then transfer the full amount to Roth IRA without any tax consequences. Note that the maximum contribution to Roth IRA is $6,000 in 2021 ($7,000 if you are 50 or above).

Roth IRA Conversion Rule Change

In 2010, the Roth conversion rule changed under the Tax Increase Prevention and Reconciliation Act of 2005 (TIPRA), repealing the AGI limit to convert traditional IRA to Roth IRA. Prior to the change in 2010, households with greater than $100,000 AGI were not eligible for a Roth conversion. In addition, if you are married filing separately, you would not be eligible for a Roth conversion.

Who benefits from Roth IRA Conversion?

Not all taxpayers will benefit from converting traditional IRA to Roth IRA. If you believe you are going to be in the same or higher tax bracket in retirement or if you are a high income professional or double income professionals phasing out to contribute to Roth IRA based on AGI, you would benefit the most from the conversion.

Most of us assume that we will be in a lower tax bracket in retirement since our income stops. This may not be necessarily true because income tax rate is subject to change in the future. In addition, if you have a large enough retirement account subject to Required Minimum Distribution (RMD) at age of 70 ½ or your lifestyle requires larger withdrawal from your retirement account before RMD, you may be in the same or higher tax bracket in retirement.

Before going through the step-by-step guide of executing backdoor Roth IRA conversion, let’s see if the backdoor Roth IRA is right for your investment strategy.

Considerations for Backdoor Roth IRA

First, do you have any existing traditional IRA, SEP RA, SIMPLE IRA? If so, review your options carefully because of the IRS “pro-rata” rule. In essence, per “pro-rata” rule, you have to account for all of your IRAs as one pool of money. Here is a simple example.

Let’s say you rolled over $50,000 in your 401(k) from a previous employer to an IRA. Now, you perform a backdoor Roth IRA with $6,000. Per the pro-rata rule, you have to add up all your IRAs, in this case, $56,000 and figure out the percentage of after-tax amount. Above the after-tax amount, the rest of the money will be taxable. In this particular example, 10.7% ($6,000 / $56,000) would be tax-free while the rest of 89.3% would be taxable. So in an attempt to convert $6,000 dollars to Roth IRA, you end up paying taxes on $50,000 which could be significant depending on your tax bracket.

So if you have any existing IRAs, use caution and consult with your tax advisor before proceeding with Backdoor Roth IRA.

Step-by-Step Guide

If you decide that a Backdoor Roth IRA is beneficial to you, here is the step-by-step guide of converting Traditional IRA to Roth IRA using Vanguard. The process is going to be mostly the same with other brokerage firms as well.

Step 1: Contribution to IRA

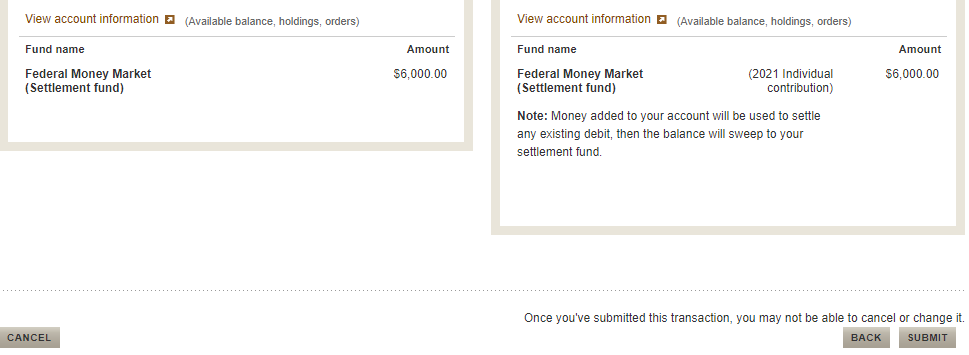

Assuming you have a brokerage account with Vanguard, the first step is to fund a traditional retirement account. Under “Buy and Sell”, choose “Contribution to IRA”.

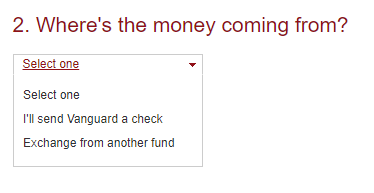

The next screen will show you details about the contribution limit. You have to answer this question: “Where is the money going?”. I typically just add it to a money market account.

You will see your contribution after you decide where the money is coming from.

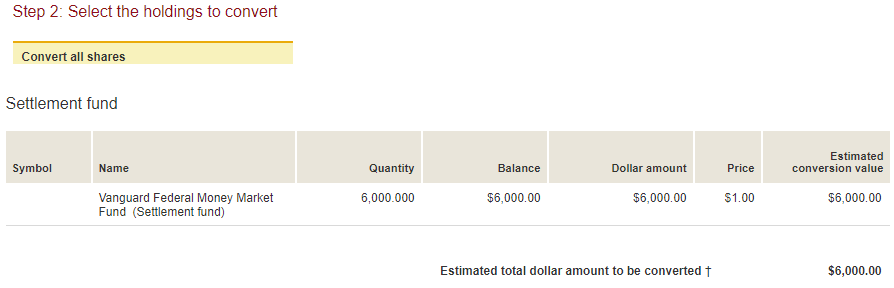

The first step of funding your traditional IRA is done. The next step is to convert to Roth IRA. I generally do it the same day to avoid any growth if any before conversion.

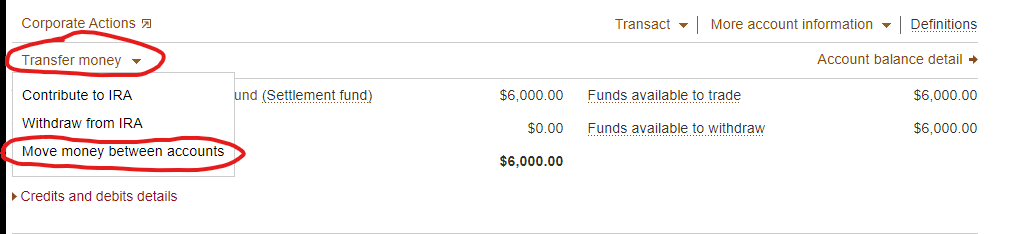

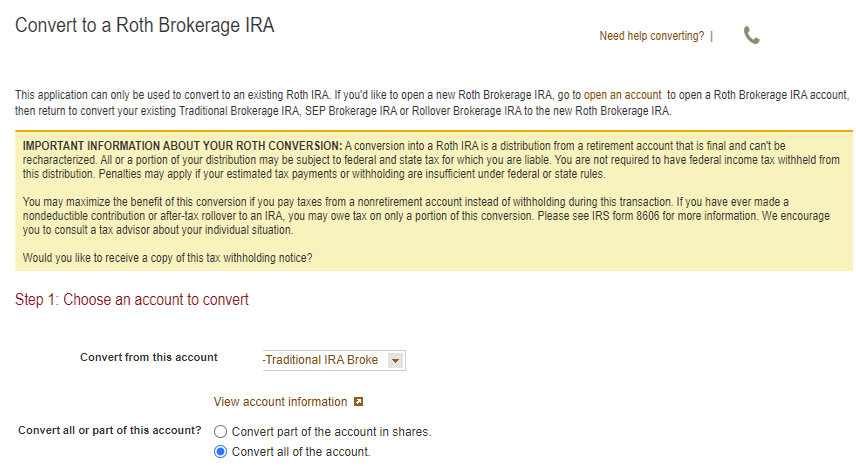

Step 2: Convert to Roth IRA

Choose your recently funded Traditional IRA account and under “transfer money” and choose “move money between accounts”

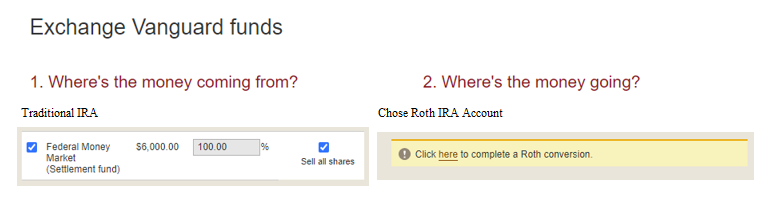

On the next screen, under “Where’s the money going” there will be an option like below. “Click” to complete Roth conversion.

Move to the next screen and pick your recently funded traditional IRA account from the dropdown list.

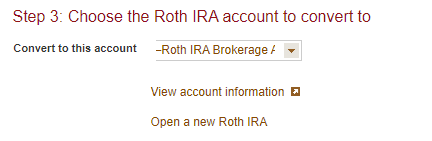

In the next screen, you have an option to choose an existing Roth IRA (if you had opened one before) or open a new Roth IRA. Choose whichever applies to you.

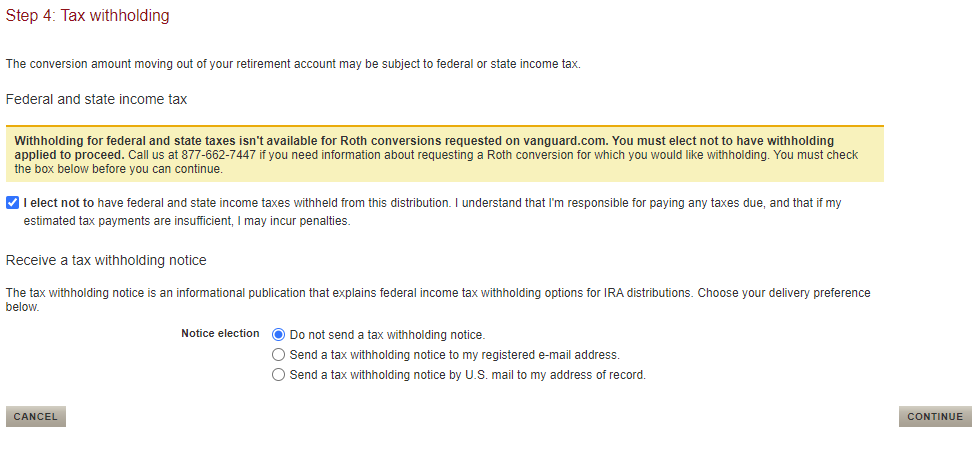

Tax Withholding Selection

The next screen will indicate that conversion of your retirement account may be subject to federal or state income tax. Since I am converting traditional IRA to Roth IRA immediately, I am not expected to owe any taxes. So I chose “Do not send a tax withholding notice”.

Click continue and you are done!

Summary

There is definitely worth considering a backdoor Roth IRA even though you cannot deduct your contributions.

- Be aware of “Pro-Rata” Rule and proceed with caution if you have existing IRAs.

- The Roth IRA has favorable tax treatment to withdraw contributions and earnings compared to traditional IRAs and other retirement plans such as 401(k).

Roth IRAs are not subject to Required Minimum Distribution (RMD).

Get our next article in your inbox.