Do’s and Don’ts of the Bear Market

Bear market declines are hard to stomach for any investor. In fact, during bear markets or during large market declines, it is a challenge to stay the course when the majority are panic selling. When you panic and sell at market bottoms you lock in losses. Hence, you would lose the ability to recover during market recovery. This article discusses do’s and don’ts to consider during bear markets or during large market declines.

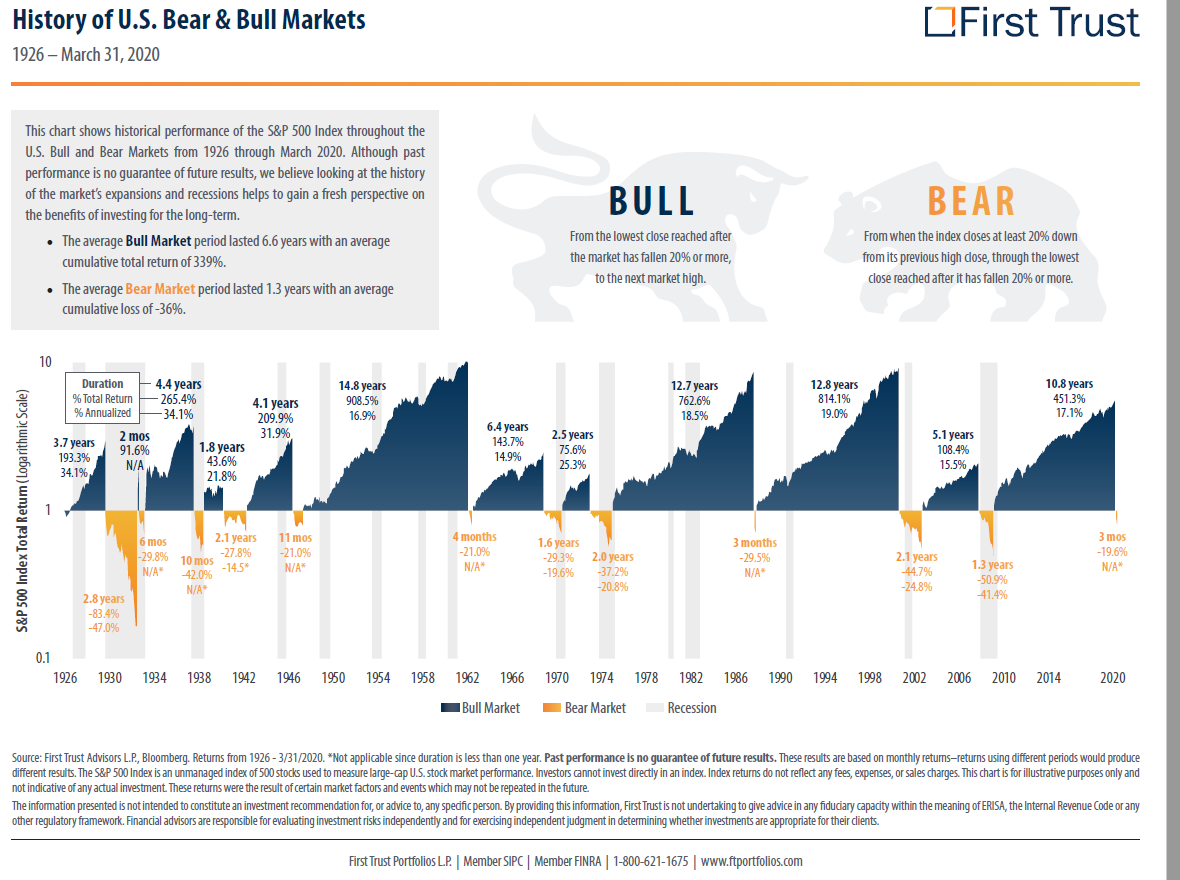

Past Bear Markets

The most recent large market decline happened in March 2020. After dropping more than 30% from its peak in March 2020, the S&P 500 index soared above 3500 in November 2020. In fact, the S&P 500 index got back to its previous high in August 2020, in just six months. Following is the S&P 500 Year-to-Date chart for 2020 (Source: fidelity.com). It is easier to see the panic selling during March 2020 would have been a mistake, right?

But what about previous bear markets or large declines? And how often should you anticipate bear markets? According to this Fidelity report, the frequency of bear market (decline of at least 20% from peak of the market) was every six years on average.

The graph from First Trust tells the story of the bear and bull market from 1926 to 2020.

Based on the First Trust data, an average bear market lasted 1.3 years with an average cumulative loss of -36%. On the other hand, an average bull market lasted 6.6 years with an average cumulative total return of 339%. Historically, bear markets were short lived, while bull markets lasted longer and generated more return than bear market losses.

So the historical data suggests that an investor with a discipline to “stay the course” is rewarded with investment gains.

Let’s crunch some numbers.

March Madness and Panic Selling

Let’s look at hypothetical investments of two investors: Joe and Paul.

Assume that Joe and Paul have 1,000 shares of Vanguard Total Stock Market Index Fund (VTSAX). Following is the value of the investment on December 31, 2019.

| Investor | Date | Quantity | VTSAX Price | Balance |

| Joe | 12/31/2019 | 1000 | $ 79.69 | $ 79,690 |

| Paul | 12/31/2019 | 1000 | $ 79.69 | $ 79,690 |

During the Pandemic, S&P 500 dropped to 2237 from its peak of 3386 on February 19, 2020. Joe did not panic and “stayed the course” while Paul panicked and sold all VTSAX shares at market bottoms.

Following is the value of investment for Joe and Paul on March 23, 2020 (bottom of the market).

| Investor | Date | Quantity | VTSAX Price | Balance | Action |

| Joe | 03/23/2020 | 1000 | $ 54.49 | $ 54,490 | None |

| Paul | 03/23/2020 | 1000 | $ 54.49 | $ 54,490 | Sold VTSAX |

So the morning of March 24, 2020 the value of Joe and Paul accounts are the same. However, Joe still owns the same amount of shares although at a lower price while Paul is out of the market without any ownership of VTSAX shares.

Market Recovery

As the market starts to recover in the June-July 2020 time frame, Paul who is on the sideline decided to go back into the market. Remember that the available balance in Paul’s account is $54,490. Paul buys the same fund VTSAX on July 31, 2020. Following is the balance of Joe and Paul investment accounts.

| Investor | Date | Quantity | VTSAX Price | Balance | Action |

| Joe | 07/31/2020 | 1000 | $ 80.57 | $ 80,570 | None |

| Paul | 07/31/2020 | 676 | $ 80.57 | $ 54,490 | Bought VTSAX |

Notice that Paul now owns 324 less shares of VTSAX than Joe. Fast forward to November 2020, following is the balance of investment account for the two investors as of November 10, 2020.

| Investor | Date | Quantity | VTSAX Price | Balance |

| Joe | 11/10/2020 | 1000 | $ 88.16 | $ 88,160 |

| Paul | 11/10/2020 | 676 | $ 88.16 | $ 59,623 |

Comparison

Following table summarizes the history of investment balance for Joe and Paul.

| Date | VTSAX Price | Quantity (Joe) | Balance (Joe) | Quantity (Paul) | Balance (Paul) |

| 12/31/2019 | $ 79.69 | 1000 | $ 79,690 | 1000 | $ 79,690 |

| 3/23/2020 | $ 54.49 | 1000 | $ 54,490 | 1000 | $ 54,490 |

| 7/31/2020 | $ 80.57 | 1000 | $ 80,570 | 676 | $ 54,490 |

| 11/10/2020 | $ 88.16 | 1000 | $ 88,160 | 676 | $ 59,623 |

By “staying the course” Joe’s return on investment is 10.6% year-to-date. However, it was not without a pain during the March 2020 market drop.

On the other hand, Paul panicked during market decline resulting in a loss of 25%. For Paul, it will take another 34% gain from November 10, 2020 to reach back the initial investment amount of $79,960. Who knows how long that would take?

Granted this is a hypothetical scenario generated from past data to make a point. However, something similar to this happens to many of us during large market declines.

What do we learn from this?

The Do’s and Don’ts

Don’t panic and sell during the bear market, stay the course instead.

However, it is easier said than done. Why? Because it is painful to watch your portfolio go down hundreds of thousands of dollars during a large market decline like in March 2020. And the bigger the portfolio, the larger the impact. For example, if you had $1,000,000 in VTSAX on December 31, 2019, it would have gone down to $683,775. That is a loss of $316,225! It is gut wrenching to see that even on the paper.

Staying the course would reward investors with the gains. In Joe and Paul’s example, Joe who stayed the course is rewarded with 10.6% gain.

Don’t sit on the sideline after the sell, tax loss harvest instead.

If this is a taxable account, the better strategy is to take advantage of “Tax Loss Harvesting”. For instance, Joe would sell the fund at loss in March 2020 and immediately invest the proceeds in a “similar” investment type to stay in the market. Thus, Paul would keep the exposure in the market and at the same time would reduce the tax burden.

You can use the loss to offset realized investment gains and up to $3,000 in taxable income. By “harvesting the loss” you save on taxes. Keep in mind, you can only use this strategy in a taxable account. This is specifically more advantageous for an investor in a high tax bracket. We will cover this in detail in future posts.

Don’t try to time the market, rebalance instead.

Market timing is not a good investment strategy. When you try to time the market, you have to be right twice; when to get out and when to get back in. In addition, market timing is not only challenging but it could reduce the rate of return of your portfolio.

Instead, rebalance your portfolio. Rebalancing is the process of re-aligning your portfolio to your set allocation. For example, let’s say that your allocation is 60% equity / 40 % bond. Due to the bear market, your allocation is now 55% equity / 45% bond. So you will “rebalance” your portfolio by selling 5% of bonds and buying stocks.

As Jack Bogle, the founder of Vanguard Group said,

Stay the course. Don’t let these changes in the market change your mind and never, never, never be in or out of the market. Always be in at a certain level.

Jack Bogle

Get our next article in your inbox.