What is Your Risk Tolerance?

Risk tolerance is defined as “an individual’s willingness to take risk when a possible outcome is negative”, according to the CFA Institute Research Foundation. In other words, risk tolerance is the willingness to accept negative outcomes in pursuit of favorable rewards in the future. The investment time horizon is one of the factors that can influence risk tolerance. For instance, an individual with a longer time horizon can be more aggressive than an individual with a similar risk profile but a shorter time horizon.

In general, the longer the time horizon, the higher the risk you can take with your investment. As your time horizon shrinks over time (moving toward retirement), it is a good idea to gradually reduce equity exposure. For instance, your investment allocation may start out with 100% stock when you are 25 years, to 60% stock / 40% bond during middle ages, to 30% stock / 70% bond in retirement.

Why do you want to reduce equity exposure as you approach retirement?

If the equity market crashes when you are young and in the accumulation phase, you will be able to purchase investment at lower price and since you do not need to withdraw money from the portfolio, it will allow your investment to recover over time. However, if the equity market crashes in early years of retirement, withdrawing money from a declining equity heavy portfolio will have a long lasting negative effect on your portfolio. This is called the Sequence of Return Risk, and it is one of the reasons to reduce equity exposure as you approach retirement. Although, you will still need 25% to 30% equity exposure in retirement to mitigate inflation risk.

How much risk are you willing to take with your investment?

Before we get into the details let’s define some terms: Realized Gain / Loss and Unrealized (“Paper”) Gain / Loss

You realize gain when you sell investment at a higher price than the purchase price. Similarly, you realize loss when you sell investment at lower price than the purchase price. You only “realize” gain or loss if you sell your investment. If you do not sell your investment, there is no gain nor loss.

The unrealized “paper” gain or loss is the fluctuation of your investment on a daily basis. As long as you do not sell the investment, the loss or gain is only on “paper”. Now, let’s get into the details.

It is one thing to read about a 40% to 50% drop in the equity market, it is another to experience actual “paper” loss of your investment. The bigger the amount, higher the impact. For example, if you have invested $10,000 dollars in an equity market, a 50% drop would be a loss of $5,000 on “paper”, still a significant amount. Now imagine your equity portfolio is $100,000, a 50% drop would be a loss of $50,000! Let’s dream big and imagine your equity exposure is $1,000,000, a 50% drop is a whopping $500,000! That is gut wrenching.

It is not easy to watch your portfolio with unrealized loss even for a short period of time.

Sure, you can answer a few hypothetical questions regarding risk tolerance; however, for most, you do not know your risk tolerance until you experience one or more “bear” markets.

Bear and Bull Market

Bear Market: According to the Securities and Exchange Commission (SEC), a bear market occurs when a broad market index such as S&P 500 or Dow Jones Industrial falls by 20% or more over at least a two-month period.

Bull Market: According to the SEC, a bull market occurs when there is a rise of 20% or more in a broad market index such as S&P 500 or Dow Jones Industrial over at least a two month period.

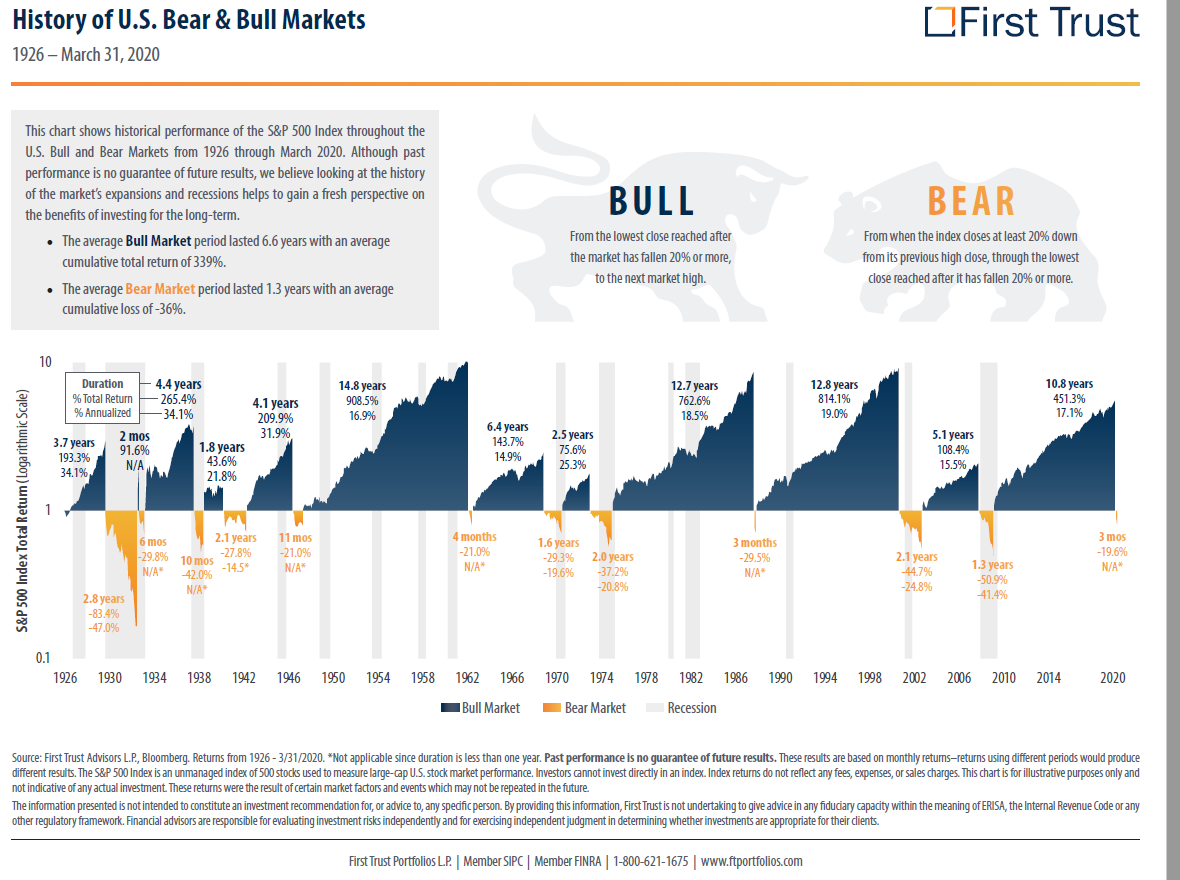

The graph (click the image to expand) from First Trust tells the story of the bear and bull market from 1926 to 2020.

Based on the First Trust data,

- An average bear market lasted 1.3 years, with an average cumulative loss of -36%. The following table lists the bear markets since 2000.

| Year | Type | S&P 500 Loss from Peak | Duration |

|---|---|---|---|

| 2001-2002 | Tech Bubble* | 45% | 2.1 Years |

| 2007-2009 | Financial Crisis | 50% | 1.3 Years |

| March 2020 | Pandemic Covid-19 | 34% | On-going |

*Nasdaq lost 78% of its value from its peak during the tech bubble.

- An average bull market lasted 6.6 years with an average cumulative total return of 339%.

History tells us that, in general, bear markets are short lived, while bull markets last longer and generate more return than bear market losses.

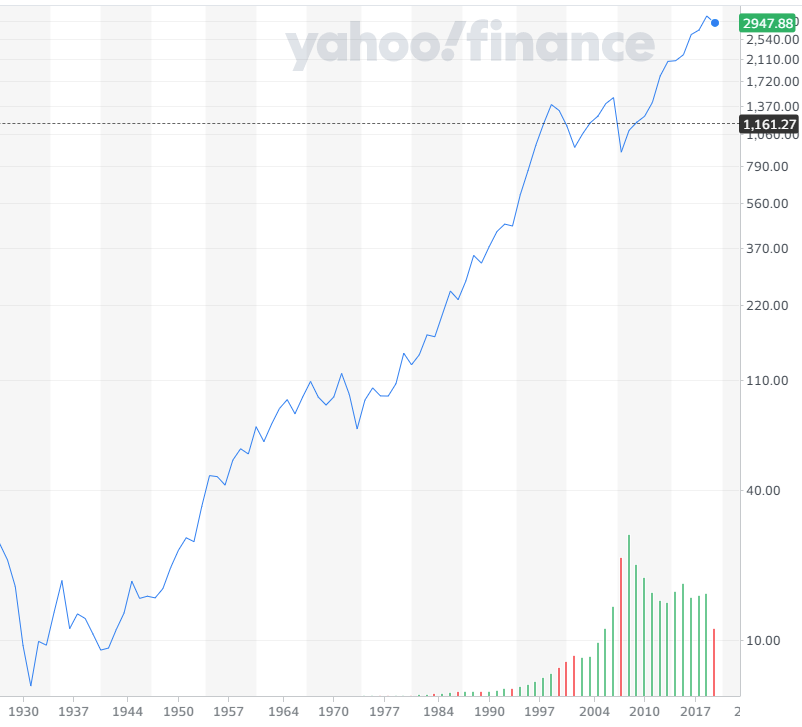

Here is the chart of S&P 500 from 1926 to May 2020 (source: Yahoo Finance).

Even with multiple bear markets – from 20% to 80% loss – the overall upward trend of the S&P 500 since 1926, suggests that equity investment may continue its upward trend over a long investment time horizon.

Will it? Nobody knows for sure. Most equity fact sheets have the following statement in one form or another: Past performance is not a guarantee of future results.

Risk Tolerance and Your Reaction

What would you do if you experience similar bear markets? Will you stick with your financial policy and do “nothing”? Will you panic and realize 50% loss on investment? If you do not sell your investment at loss, will you be worried sick, consequently impacting your health?

What is your willingness to accept a negative outcome, a temporary “paper” loss, in pursuit of favorable rewards in the future? The answer to that question is how you would define your risk tolerance, your “sleep at night number”, regardless of your age.

So, how do you decide what your risk tolerance is when you are just starting out? I recommend going through the Investor Questionnaire by Vanguard to get a general idea about your risk tolerance and your initial allocation.

If you are risk averse, I recommend starting with a classic 60% stock / 40% bond allocation and stick with it through bull and bear markets.

As Jack Bogle, the founder of Vanguard Group (world’s largest mutual fund firm) said,

Stay the course. Don’t let these changes in the market change your mind and never, never, never be in or out of the market. Always be in at a certain level.

Jack Bogle

What is your risk tolerance? What did you do during past bear markets?